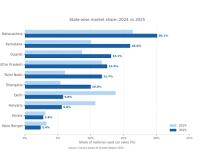

The statistical rebalancing is underscored by a sharp decline in traditional strongholds alongside unprecedented gains in emerging markets. Delhi’s national sales share plummeted from 13.8 percent in 2024 to a mere 5.8 percent in 2025, while Haryana witnessed a similar contraction from 10.7 percent to 5.6 percent. In stark contrast, Maharashtra consolidated its status as the premier market, growing from 16.4 percent to 20.1 percent. Karnataka surged from 10 percent to 16 percent, and Gujarat climbed from 8.7 percent to 13.1 percent, while Tamil Nadu and Telangana effectively doubled their market presence. This geographic diversification indicates that the market is now drawing from a robust base across western, southern, and central India rather than being tethered to northern metropolitan consumption patterns.

Analytical data reveals that metro and non-metro buyers operate on entirely different demand profiles. Metro consumers, who account for 38 percent of sales, are primarily "upgraders" treating the used car market as an aspirational ladder to acquire SUVs and premium hatchbacks. These urban buyers seek lifestyle-driven features like automatic transmissions and maintain shorter ownership cycles. Conversely, the 62 percent of buyers in Tier-2 cities are largely first-time owners motivated by functional needs, including reliability, fuel efficiency, and low maintenance. This segment favors hatchbacks and compact sedans, prioritizing durability and resale value over stylistic trends. Furthermore, financing adoption is notably higher in non-metro areas at nearly 58 percent, compared to 50 percent in metros, reflecting the efficacy of digital lending platforms in reaching smaller urban centers.

Model preferences further highlight these divergent priorities. While the Tata Nexon maintains its position as the top-selling vehicle across both geographies with approximately 4 percent share, the secondary rankings vary significantly. Metros favor the premium Baleno in second place, whereas Tier-2 markets prefer the Hyundai Grand i10 for its widespread service network and affordability. The Honda City remains a staple in the metro top ten but is entirely absent from the non-metro list, where the entry-level Renault Kwid ranks fourth due to its low cost of ownership. Spending patterns also fluctuate by state, with Tamil Nadu leading at an average selling price of Rs 5.49 lakh, driven by premium demand, while Uttar Pradesh reflects a value-first approach with an average price of Rs 4.90 lakh.

Three primary forces are propelling this Tier-2 ascendancy: rising incomes among salaried and self-employed households, the elimination of the trust gap through digital inspection platforms, and increased SME activity. In states like Gujarat, vehicles often serve the dual purpose of family transport and trade-driven utility, creating a consistently motivated demand base. This evolution confirms that Tier-2 India is not merely catching up to metropolitan standards but is instead constructing an independent, resilient market. As digital financial infrastructure continues to expand, the national used car industry has become more stable, ensuring that the aspirations of a widespread middle class now dictate the future of Indian automotive commerce.

About The Author

Comment List